THIRD QUARTER INSIGHTS – September 2, 2025

PERCEPTIONS

by LESLIE CALHOUN, President and CEO

In a subtle but significant move, Federal Reserve Chair Jerome Powell recently hinted at a change in the central bank’s approach to U.S. monetary policy. At the Jackson Hole symposium, Powell acknowledged that job growth is slowing and that risks to employment are “rising.” He also noted that the “shifting balance of risks may warrant adjusting our policy stance.”

This change in tone has already impacted markets, which are now largely expecting a 25-basis-point rate cut at the September Federal Open Market Committee (FOMC) meeting. Since their rate hikes began in 2022, the Fed’s restrictive policy was justified by high inflation, but now, the growing risk of unemployment is challenging that stance.

By easing its policy, the Fed is not only addressing potential employment issues but also trying to prevent a “hard landing” for the U.S. economy. Recent data supports this move, showing a “soft landing” scenario where the economy is cooling down without collapsing, and inflation is retreating from last year’s highs.

The Fed’s potential pivot isn’t happening in isolation. Central banks around the world, from Europe to Asia, are also cutting rates. This synchronized global easing could provide a tailwind for both global growth and various assets. Additionally, this trend could also put downward pressure on the U.S. dollar, which could be good news for non-U.S. dollar assets.

While a rate cut in September seems likely, the Fed’s next moves will depend on upcoming data. If job growth, wage increases, or inflation surprise to the upside, the Fed might opt for a “hawkish cut”—cutting rates while signaling that further easing will be shallow. This could paradoxically tighten financial conditions, as it might lead to a rise in long-term interest rates.

Ultimately, the path forward is uncertain and will be driven by data. Market participants should be cautious and not assume that a rate cut is the start of a full-blown easing cycle. The Fed’s balancing act between managing inflation and employment is becoming more challenging than ever.

sweeping changes to federal estate tax laws take effect

by MATT McMANUS, Wealth Advisor and COO

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, makes significant and permanent changes to federal estate, gift, and generation-skipping transfer (GST) tax exemptions. This new law provides clarity by making key tax provisions permanent but necessitates a review of existing estate plans.

What has changed?

1. Increased and permanent exemptions

The OBBBA eliminates the “sunset” provision of the 2017 Tax Cuts and Jobs Act, which would have reduced estate and gift tax exemptions at the end of 2025.

- For 2025: The exemption is $13.99 million per individual, or $27.98 million for a married couple.

- Starting January 1, 2026: The base exemption increases to $15 million per individual, or $30 million for a married couple, indexed for inflation.

- GST Exemption: The GST tax exemption is also permanently increased to align with the estate and gift tax exemption.

- Relief for individuals and couples

The higher exemption significantly reduces the number of estates subject to federal estate tax and offers greater flexibility for wealth transfer strategies, particularly for high-net-worth individuals. The IRS has confirmed it will not “claw back” gifts made between 2018 and 2025 that exceeded the pre-TCJA exemption. - Annual gift tax exclusion

The annual gift tax exclusion increases to $19,000 per recipient for 2025. - Income tax basis

The “step-up in basis” rule at death is retained, allowing an heir’s cost basis to be the asset’s fair market value at the time of the owner’s death.

What should you do now?

While the immediate pressure to act before the end of 2025 is gone, individuals should still review their estate plans and consider some of the following wealth transfer strategies.

As trusts are a cornerstone of advanced estate planning, using the increased exemptions with trusts is a primary strategy for wealth transfer and asset protection. Consider some of the following trust structures.

Strategic Trust Structures

- Dynasty Trusts: These irrevocable trusts can last for multiple generations and are exempt from gift, estate, and generation-skipping transfer taxes. The assets in the trust grow tax-free, and distributions can continue to benefit descendants for many decades.

- Spousal Lifetime Access Trusts (SLATs): A SLAT allows one spouse to make a substantial gift to an irrevocable trust for the benefit of the other spouse and other family members. The gift uses the donor spouse’s lifetime exemption, removing the asset and all its future appreciation from their taxable estate. Since the beneficiary spouse has access to the funds, this strategy offers flexibility for couples concerned about relinquishing control of assets.

- Grantor Retained Annuity Trusts (GRATs): A GRAT is an irrevocable trust used to transfer appreciating assets. The grantor receives a fixed annuity payment from the trust for a set term. Any remaining assets at the end of the term, including all appreciation above an IRS-mandated interest rate, pass to beneficiaries tax-free.

- Intentionally Defective Grantor Trusts (IDGTs): An IDGT allows a grantor to “freeze” the value of assets for estate tax purposes by selling appreciating assets to a trust in exchange for a promissory note. The grantor pays the income taxes on the trust’s income, allowing the trust assets to grow income-tax-free for the beneficiaries.

Lifetime gifting strategies

With the exemptions now permanent at a higher level, lifetime gifting remains a powerful tool to transfer wealth out of a taxable estate.

- Maximize annual exclusion gifts: For 2025, individuals can give up to $19,000 per recipient without affecting their lifetime exemption. Married couples can combine their exclusions to gift $38,000 per recipient. These gifts can be made annually to multiple people, steadily reducing the size of the taxable estate.

- Utilize the full lifetime exemption: Individuals with substantial wealth can now confidently make large gifts using their full lifetime exemption (over $15 million in 2026, indexed for inflation) without fear of a future “claw back” when exemptions drop.

- “Superfund” 529 plans: As part of a gifting strategy, individuals can front-load up to five years of annual gift tax exclusions into a 529 college savings plan. For 2025, this is $95,000 per beneficiary, or $190,000 for married couples.

Charitable planning

Philanthropic vehicles offer another way to transfer wealth while providing tax benefits.

- Charitable Remainder Trusts (CRTs): By contributing assets to a CRT, a grantor receives a tax deduction and an income stream for a specified term. The remaining assets are passed to a charity, effectively reducing the taxable estate.

- Donor-Advised Funds (DAFs): This flexible tool allows for a lump-sum charitable contribution with an immediate tax deduction, while the donor retains the ability to recommend grants to different charities over time.

Family entities and business succession

- Family Limited Partnerships (FLPs) or LLCs: High-net-worth families often use these entities to transfer interests in family businesses or real estate to younger generations. By gifting minority or non-voting interests, families can take advantage of valuation discounts, allowing them to transfer more wealth using less of their lifetime exemption.

With the passage of the OBBBA, there is now far more clarity than we’ve had over the last 8 years. With that clarity brings into focus a number of strategies that can help protect your assets. With the assistance of an estate planning attorney, we can help you navigate the complexities of protecting your hard-earned wealth today and for generations to come.

the new energy revolution

by RYAN THOMASON, CFA, Portfolio Manager

As we navigate an era of profound transformation in the US energy landscape, it’s clear that we’re on the cusp of a multi-decade opportunity. After years of stagnant growth, electricity demand is surging at an unprecedented rate, driven by structural forces that extend far beyond the buzz around artificial intelligence and data centers. This “thirst for power” isn’t just a headline – it’s a fundamental shift reshaping industries, economies, and investment portfolios.

There are many underappreciated drivers of demand for this energy revolution. Data centers certainly grab the spotlight, as many cities and utility companies race to figure out how to produce the power these data centers require. They represent about a third of the projected annual growth in US power demand through 2030. This isn’t a meaningless number, but there is more to this demand than just data centers. The real story lies in the broader resurgence of manufacturing, the electrification of everyday life, and the transition to electric mobility. These three collectively account for the lion’s share of this expansion.

- Reindustrialization and Onshoring: For the first time in decades, US industrial power consumption is on the rise. Globalization’s offshoring trend is reversing, fueled by a focus on supply chain resilience and bipartisan policy support. Since early 2021, over $1.8 trillion in mega-projects have been announced, with the majority yet to break ground. This spans from semiconductors, petrochemicals, and automotive production, and has the potential to drive industrial demand growth of up to 3% annually through 2035.

- Electrification of Homes and Businesses: Efficiency and cost savings are accelerating the adoption of electric technologies in residential and commercial spaces. Heat pumps, electric appliances, and air conditioning are becoming mainstream and standard, supported by falling costs, utility incentives, and rebates. This shift isn’t just about convenience – it’s a structural move toward lower operating expenses and greater resilience, steadily increasing baseline electricity use.

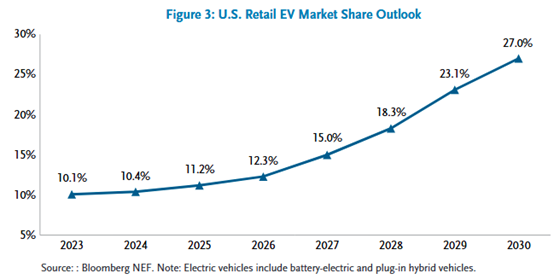

- The Rise of Electrical Transportation: Electrical vehicles (EVs) are poised to capture 27% of the US auto market by 2030, up from around 10% today. Advances in battery technology, charging infrastructure, and incentives at state and local levels are overcoming hurdles, even amid federal policy fluctuations. This growth will add significant load to the grid, particularly during peak evening hours, necessitating upgrades in infrastructure and smart systems.

As demand accelerates, supply is struggling to keep up. New generation capacity –from renewables to traditional sources – faces regulatory and logistical challenges, leading to tighter markets. In some regions, electricity prices are already climbing by as much as 20%, enhancing the profitability of power generation, grid solutions, and essential equipment. This imbalance is creating bottlenecks but also unlocking value. The US grid, long overdue for modernization, now requires trillions in capital for transmission, distribution, and reliability enhancements. Nuclear and natural gas, which are reliable 24/7 sources, are gaining renewed appreciation, while industries like electrical equipment and critical materials stand to benefit immensely.

This energy revolution is more than a sector story; it’s a generational theme ripe for investment across equity, credit, and infrastructure. “Old economy” players in utilities, power equipment, and industrials –often overlooked in favor of technology darlings – are emerging as new market leaders. Their fundamentals are strengthening amid rising demand and pricing power, offering diversification and potential for outsized returns.

In a world fixated on AI, the true power play lies in these underappreciated forces. By aligning with and investing in this thematic, investors can capture resilient growth, hedge against volatility, and contribute to a more secure energy future.

Respectfully,

Leslie, Matt, Ryan & Ashlee