FOURTH QUARTER INSIGHTS – December 4, 2025

PERCEPTIONS

by LESLIE CALHOUN, Senior Partner and CEO

As we look into the end of 2025, the US equity market remains a leader globally, supported by strong earnings and consumer spending. The market is buoyed by earnings upgrades, resilient consumer spending, and strong corporate balance sheets. Continued disinflation and potential gradual Fed easing provide a supportive backdrop for equities and real assets. Our biggest concern seems to be the same as the Federal Reserve’s, unemployment creeping up as more companies announce workforce reductions and have fewer job openings.

The ultimate impact of rate cuts will take time, but expectations for the benefits to flow, both to the consumer and overall economy, are in focus. For the consumer, lower borrowing costs should be a benefit, particularly with a decline in credit card rates combined with tax relief. With changes to the U.S. tax code, including auto loan interest deductions and the removal of taxes on overtime and tips, consumers should see at least a modest increase in spending power by early 2026. Time will tell if rate cuts result in lower mortgage rates, which would also be positive. Meanwhile, on the business side, the lower borrowing costs, combined with deregulation and investment incentives, such as accelerated depreciation, could spur incremental domestic investments.

We are encouraged that all the previously mentioned factors will lead us to finish strong in the 4th quarter and set the stage for a positive 2026. However, if there are any changes to the expectations of continued fed cuts or any additional geopolitical conflicts, that could easily cause disruption to our projections.

Navigating Conflicting signals

by RYAN THOMASON, CFA, Portfolio Manager

As we begin the final month of the year, investors are facing conflicting signals. The S&P 500 reached new all-time highs in the fourth quarter, as markets continued to be supported by strong corporate earnings. At the same time, the labor market has weakened since the beginning of the summer, raising concerns over the underlying economy and the financial health of consumers. We have also seen enthusiasm for artificial intelligence start to wane, as investors begin to question what return on investment will be seen after billions have been invested into semiconductors and data centers. Despite this, GDP growth has been strong, and inflation has largely stayed in check.

Market environments like these are precisely when the benefits of long-term investing and financial planning shine. Rather than reacting to headlines and economic reports, it is important to hold well-constructed portfolios that can withstand market shifts. This requires understanding the underlying trends that will shape markets in the quarters ahead.

Key Market and Economic Drivers in October

- The S&P 500 rose slightly by 0.1% in November, the Dow Jones Industrial Average gained 0.3%, and the Nasdaq declined 1.5%. Year-to-date, the S&P 500 is up 16.4%, the Dow is up 12.2%, and the Nasdaq is up 21.0%

- The Bloomberg U.S. Aggregate Bond Index rose 0.6% in November and is now up 7.5% year-to-date. The 10-year Treasury yield ended the month lower at 4.02%, after briefly falling under 4%.

- The VIX, a measure of stock market volatility, finished lower at 16.35 after climbing as high as 26.42 mid-month.

- International developed markets, as measured by the MSCI EAFE index, rose 0.5% in U.S. dollar terms and emerging markets, as measured by the MSCI EM index, fell 2.5%% in November. Year-to-date, they have returned 24.3% and 27.1%, respectively.

- Gold prices ended the month higher at $4,218, but still below the October all-time high of $4,336.

- Bitcoin experienced a significant decline of about 17% in November, ending the month at $91,176.

- The U.S. Dollar Index ended the month at 99.46 and briefly crossed the 100 level.

- The September jobs report, which was delayed due to the government shutdown, showed that the economy added 119,000 new jobs and the unemployment rate ticked higher to 4.4% that month. There will be no October jobs report.

Valuations

AI bubble fears have resurfaced with heightened intensity. Critics and bears cite soaring valuations for AI-linked companies, unprecedented capital pouring into infrastructure (such as data centers and semiconductors), and a growing web of interdependent deals among model developers, cloud giants, and hyperscalers that increasingly blur the lines between partners and providers. These dynamics are reminiscent of past manias like the Dot-Com era, raising questions about whether the market surge is masking underlying fragility.

Unlike the Dot-Com days, there are notable differences that should temper the alarms. Public market valuations and deal activity lag far behind the Dot-Com highs, and the “Magnificent Seven” tech leaders continue to churn out robust free cash flow, execute stock buybacks, and issue dividends—hallmarks absent in prior bubbles. The U.S. equity market isn’t in a full-blown bubble yet, as earnings growth data shows profits have been keeping pace with prices (unlike the Dot-Com era). As time goes on, pundits and bears will continue to scrutinize this market rally as valuations approach levels last seen during the Dot-Com boom-bust. Yet the environment is different, and a simple comparison from a valuation standpoint doesn’t justify the same fate. Fundamentally, this market still has room to run, albeit with heightened volatility.

We have already seen these fears impact market returns, with risk assets such as technology stocks, high-yield bonds, cryptocurrencies, and other investments experiencing their worst week since April. There have now been six declines of 5% or worse for the S&P 500 this year, the most since 2022 but still close to the historical average of 4.6. Some major asset classes rebounded in the final days of the month, and the S&P 500 ended slightly positive.

While the S&P 500 and Nasdaq continue to outperform other indexes and risk investments, as stewards of capital, it is our responsibility to remain diversified and allocate capital in other areas of the market that appear undervalued. For example, we have recently increased our allocations to mid-cap stocks, value stocks, and international stocks, as they have more attractive valuations and differentiated tailwinds that should propel those areas forward. Lastly, we have begun allocating to private equity, as many successful companies have decided to stay private for longer.

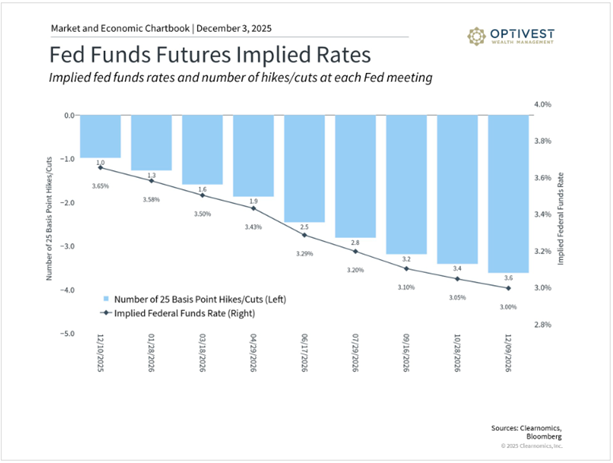

Market Expectations for the Next Fed Rate Cut Have Shifted

The Bureau of Labor Statistics released the long-awaited September jobs report, which was originally scheduled to be published in October. This report showed that job gains exceeded expectations that month, rebounding from weakness over the summer. However, the revised figures show that 4,000 jobs were lost in August, the second month of negative jobs growth this year. The unemployment rate edged up to 4.4% in September, its highest level since September 2021, although this is still low by historical standards.

A full October jobs report will not be published because of the government shutdown, but some of the data will be included in November’s report. This data delay means that the Federal Reserve will enter its mid-December meeting without a full economic picture. Expectations for a rate cut at the next Fed meeting have shifted dramatically, with the probability dropping in mid-November before rebounding once again. At the moment, the market-based expectations suggest the Fed will cut rates in December and then again in April or June 2026.

Beyond policy rates, the Fed also announced it would stop shrinking its balance sheet in December. This means they will reinvest proceeds from maturing securities, effectively maintaining supportive monetary policy. Over the past three years, the Fed has tightened policy by reducing its balance sheet by $2.2 trillion; ending this process provides additional economic support. For investors, declining interest rates and supportive monetary policy have historically provided tailwinds for both stocks and bonds, provided the economy remains strong.

Respectfully,

Leslie, Matt, Ryan & Ashlee