SECOND QUARTER INSIGHTS – April 24, 2026

PERCEPTIONS

by LESLIE CALHOUN, Senior Partner and CEO

The latest data are showing a common pattern so far: inflation has re-accelerated on energy and tariff effects, while labor markets remain reasonably intact.

Rates, Inflation, Growth, and Geopolitics

The broad macro story has shifted from “disinflation with falling rates” to “still-expanding growth, but with renewed inflation pressure and more cautious central banks.” The main reason is not a collapse in labor markets; in most major economies, employment is still holding up reasonably well. Instead, the pressure is coming from energy, trade frictions, and the uncertainty created by the Iran war and changing tariff policy. The IMF’s April outlook now frames 2026 as a year of slower but still positive growth under a limited-conflict assumption, with downside risk if energy disruption persists.

In the US, the Fed held its policy rate at 3.50% to 3.75% in March. At the same time, the labor market remains softening-but-stable: March payrolls rose 178,000 and unemployment held at 4.3%. Inflation, however, moved back the wrong way in March, with headline CPI at 3.3% year over year and core CPI at 2.6%, driven in part by a sharp rebound in energy prices. That combination argues for patience from the Fed rather than urgency to cut. Growth still looks positive, but slower than last year: the Atlanta Fed’s GDPNow estimate for Q1 was 1.3%, while the IMF’s 2026 U.S. growth forecast is 2.3%.

For U.S. investors, the key swing factors are oil, tariffs, and diplomacy. Fed Governor Christopher Waller said last week that tariffs had materially boosted measured inflation, even as tariff-adjusted underlying inflation looked closer to 2%. Meanwhile, the IMF says the current U.S. tariff regime is lighter than the harsher path assumed last fall because of court rulings and executive actions, but trade policy uncertainty remains high. On the geopolitical side, the fragile U.S.-Iran ceasefire and repeated disruptions around the Strait of Hormuz have kept oil markets volatile, with Brent recently back near the mid-$90s. For the U.S., that likely means growth continues, but at a more modest pace, with inflation staying stickier than many hoped and rate cuts harder to justify quickly.

The euro area faces a tougher setup. The ECB is holding its key rates at 2.00%. Euro area inflation rose back to 2.6% in March from 1.9% in February, with energy inflation at 5.1%, while unemployment in February was still relatively low at 6.2%. That means Europe has not entered recession, but it also has not regained enough momentum to absorb a fresh energy shock comfortably. The IMF now projects euro area growth of just 1.1% in 2026.

Europe is especially exposed to the Iran conflict because it remains a major energy importer, and recent IMF commentary explicitly points to weaker investment and consumption as energy costs rise again. Trade is another headwind: EU exports to the United States fell by more than a quarter year over year in February for a second straight month, although some of that drop reflects payback after earlier front-loading. In plain English, Europe looks like the major region with the least margin for error: diplomacy that restores energy flows would help quickly, but a prolonged conflict or wider tariff escalation would likely keep growth subdued and inflation uncomfortably above target.

Asia ex-China is a diverse region, so there is no single policy rate. Even so, the regional pattern is clear: growth is still better than in the West, but energy-importing economies are newly vulnerable. The IMF’s Asia-Pacific outlook projects regional growth of 4.4% in 2026 and 4.2% in 2027, while inflation rises to 2.6% this year from 1.4% last year because of the energy shock. Policy settings remain mixed: Japan’s policy rate is about 0.75%, South Korea’s base rate is 2.50%, and Australia’s cash rate is 4.10%. In Japan, CPI was 1.3% in February and unemployment 2.6% so slow and steady remain the theme.

The investment takeaway for Asia ex-China is that the region still has the best growth profile outside the U.S., but it is also highly sensitive to oil and shipping disruption. Countries such as Japan, Korea, Thailand, and Vietnam benefit quickly from calmer diplomacy and lower energy prices; they also feel pain faster when Hormuz risk rises. So the base case is still expansion, but with more inflation volatility and more uneven central-bank paths than we expected a few months ago.

China looks somewhat different from the rest of Asia. Its benchmark loan prime rates were left unchanged again today at 3.00% for the one-year tenor and 3.50% for the five-year tenor. Their inflation remains low by global standards: March CPI was 1.0% year over year, with core CPI at 1.2%. Their published unemployment rate averaged 5.3% in Q1 2026. Yet growth has held up better than many expected, with 5.0% real GDP growth in the first quarter.

That leaves China in a relatively strong but still incomplete recovery. Low inflation and steady policy rates suggest Beijing still has room to stay supportive through stimulative policy if external demand weakens or geopolitics worsen. China is not immune to the Iran war or to tariff friction, but compared with Europe and much of Asia ex-China, it appears somewhat better buffered for now by policy flexibility, strategic preparation, and firmer recent domestic data. The most likely path is still moderate growth rather than a reacceleration boom.

Dynasty Trusts & the OBBBA Window of opportunity

by MATT McMANUS, M.A., CFP®, Partner

What is a Dynasty Trust?

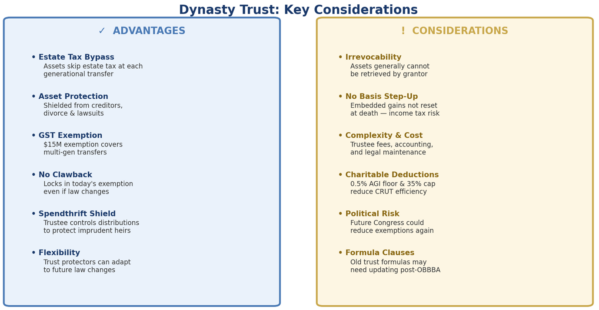

A dynasty trust is an irrevocable trust designed to hold and grow family wealth across multiple generations — sometimes in perpetuity — rather than distributing assets outright to heirs at a fixed point in time. The grantor funds the trust, a professional trustee manages distributions at their discretion, and a broad class of current and future beneficiaries can benefit over decades and generations.

The key legal enabler is the abolition or relaxation of the Rule Against Perpetuities (RAP) in favorable trust jurisdictions. States such as South Dakota, Nevada, Delaware, and Alaska have abolished the RAP entirely — allowing truly perpetual trusts. Importantly, you do not need to reside in these states to take advantage of their laws; the trustee simply needs to be domiciled there.

At its core, a dynasty trust accomplishes three things simultaneously:

- Estate Tax Bypass: Removes assets from your taxable estate while allocating your Generation-Skipping Transfer (GST) exemption — allowing wealth to pass through multiple generations without additional estate tax.

- Asset Protection: Keeps assets beyond the reach of beneficiaries’ creditors, divorcing spouses, and civil judgments.

- Spendthrift Protection: Maintains trustee control over distributions, protecting heirs from their own financial decisions while still providing for their needs.

What Changed Under the OBBBA?

Prior to the OBBBA, the elevated estate tax exemptions from the 2017 Tax Cuts and Jobs Act (TCJA) were scheduled to sunset on January 1, 2026 — cutting the per-person exemption from approximately $13.99 million to roughly $7 million. That cliff is now gone.

The OBBBA’s most significant estate planning provisions, effective January 1, 2026, are:

The elimination of the sunset is as important as the exemption increase itself. Advisors and clients can now plan with confidence over multi-year and multi-generational horizons — without fear that a legislative deadline will suddenly change the calculus.

Why Dynasty Trusts – and Why Now?

Even with permanent higher exemptions, the window to act is not unlimited. Here is why clients with significant estates should be moving now:

Political risk remains the most important reason to act promptly. While the OBBBA made the exemption “permanent,” that designation is only as durable as the current Congressional majority. A new administration or Congressional realignment — potentially as early as 2027 following midterm elections, or 2029 following the next presidential election — could revisit these provisions.

Additionally, clients who previously used their full TCJA exemption may now have headroom to make additional gifts. A married couple who each used $13.99M in prior years now has approximately $1.01M per person — $2.02M combined — in additional available exemption to fund a dynasty trust or top off an existing one before the opportunity shifts.

Finally, the OBBBA also introduced new limitations on charitable deductions beginning in 2026 — including a 0.5% AGI floor and a cap on deduction benefits for top-bracket taxpayers. Clients who planned to pair a dynasty trust with a Charitable Remainder Trust (CRUT) or Donor-Advised Fund (DAF) should know that the income tax efficiency of those charitable components has decreased. This further reinforces the value of locking in pure estate planning vehicles — like the dynasty trust itself — while the exemptions and broader planning environment remain favorable.

The Compounding Power of Multi-Generational Planning

Perhaps the most compelling case for a dynasty trust is the simple mathematics of compound growth, uninterrupted by estate taxation at each generational transfer.

Consider a family that funds a dynasty trust with $15 million today — fully utilizing the new OBBBA exemption — invested at a hypothetical 6% annual return. Compared to an equivalent taxable estate that faces a 40% estate tax at each generational transfer (approximately every 25 years), the long-run wealth difference is substantial:

Over 50 years, the dynasty trust in this hypothetical grows to approximately $276 million, compared to roughly $172 million in the taxable scenario — a difference of over $100 million attributable primarily to the avoidance of one generational estate tax event. Across three or four generations, this disparity becomes transformational.

Weighing the Tradeoffs

Dynasty trusts are powerful — but not without meaningful tradeoffs. A complete planning conversation requires an honest assessment of both sides:

The most significant tradeoff to understand post-OBBBA is the basis step-up issue. Assets held inside an irrevocable dynasty trust generally do not receive a step-up in income tax basis at death — meaning embedded capital gains on appreciated assets remain locked in and will be taxed when the trust eventually sells those positions. With federal estate tax now less of a concern for many families (given the $15M exemption), income tax planning has become the dominant consideration in structuring. For clients with highly appreciated assets, carefully modeling the estate tax savings against the foregone basis step-up is essential before committing assets to a dynasty trust.

Additionally, existing trusts and wills that use formula clauses tied to prior exemption amounts should be reviewed. Documents drafted under TCJA assumptions — where the sunset was a real planning factor — may now operate differently than intended, potentially overfunding certain trust sub-accounts or misallocating assets among beneficiaries.

Who is the Ideal Candidate?

Dynasty trusts are not one-size-fits-all. They tend to deliver the greatest value for clients who meet several of the following criteria:

- Estate significantly exceeding $15M (single) or $30M (married) — where federal estate tax remains a real exposure

- Assets with strong appreciation potential that benefit most from compound growth unencumbered by generational estate taxes

- Concerns about heir financial discipline, creditor exposure, or marital instability in the next generation

- A genuine desire to build multi-generational family wealth rather than simply transfer assets

- Business succession needs — where control and ownership transfer over time, with the trust as a long-term holding vehicle

Clients in the $7M–$15M range who want to protect assets from potential future exemption reductions — the no-clawback rule makes this particularly compelling for those who can act now

Choosing the Right Jurisdiction

The state in which a dynasty trust is established — its “situs” — matters significantly for both the duration of the trust and its asset protection strength. The following states are the most commonly used for dynasty trust planning and each offer distinct advantages:

California residents have no state estate tax, but California does impose income tax on trusts with California trustees or California-resident beneficiaries. Careful trustee selection and siting of the trust in a favorable jurisdiction can significantly reduce ongoing state income tax on trust earnings, compounding the long-run benefit.

Your Next Steps

The OBBBA has created one of the most favorable estate planning environments in recent memory — but the window is not indefinitely open. Political risk, changing exemption amounts, and individual tax circumstances all argue for proactive planning in 2026. Here is how to think about next steps:

- Schedule a planning review with Optivest to assess your current estate exposure under the new $15M exemption framework.

- Model the tradeoffs between dynasty trust funding and the basis step-up — particularly for those of you with significant unrealized gains in appreciated real estate or concentrated stock positions and determine what assets may be best gifted to the dynasty trust.

- Review existing wills, trusts, and beneficiary designations for formula clauses that may operate differently under current law.

At its heart, a dynasty trust is not simply a tax strategy — it is a declaration of intent. It is a decision to think beyond your own lifetime, to ensure that the wealth you have spent decades building continues to work for your children, your grandchildren, and the generations that follow. Assets held inside a well-structured dynasty trust compound uninterrupted across generations, shielded from estate taxes, creditors, and the financial vulnerabilities that so often erode family wealth over time. The OBBBA has made this kind of long-horizon planning more accessible and more certain than ever before. If you have ever asked yourself what kind of legacy you want to leave — not just what you will pass on, but how it will be protected and grown for those who come after you — a dynasty trust may be one of the most powerful answers available to you. We invite you to start that conversation with us.

The Fundamentals still win: navigating markets amid middle east tensions

by RYAN THOMASON, CFA, Portfolio Manager

Markets Reach New Highs Amid Ongoing Political Uncertainty

The ongoing conflict between the United States and Iran continues to drive market movements, but there’s an encouraging headline worth noting: the S&P 500 has climbed back to positive territory for the year, reaching a new all-time high after a dip in March. While that’s welcome news, the path to get here has been anything but smooth – and the situation in the Middle East continues to evolve in ways that warrant close attention.

Markets Have Rebounded, But Volatility Remains

Improving sentiment around the Iran conflict has been a key catalyst behind the S&P 500 surpassing its previous peak from January. Investors are increasingly hopeful that greater regional stability could eventually reopen the Straight of Hormuz, easing pressure on energy markets. Iran’s latest declaration around reopening the Straight of Hormuz has been a welcoming sign, yet they continue to go back and forth on the terms, leading to the United States declaring their own blockade on the straight. This is further complicated by a ceasefire that had expired and then was ultimately extended indefinitely.

Over the past six weeks, markets have swung in both directions as headlines have shifted. Oil prices, which briefly spiked above $100 per barrel, have since pulled back into the $80-$90 range. The ceasefire, while encouraging, did not produce a lasting peace deal, leading to heighted uncertainty. That said, there are now expectations that the U.S. and Iran could return to the negotiating table in the coming weeks – though unresolved issues, including the future of Iran’s nuclear program, make a swift resolution far from guaranteed.

One reason markets have rebounded as quickly as they have is that the underlying fundamentals of public companies remain healthy. Strong corporate earnings have supported the rally, with S&P 500 earnings-per-share growth running above 15% – well above the long-term historical average of 7.7%. Broad market valuations have risen alongside the rebound, with the S&P 500 price-to-earnings ratio back above 20x, though still below the elevated levels seen in recent years.

Inflation Bears Watching, But Hasn’t Broadened – Yet

The March Consumer Price Index (CPI) report showed the most direct impact of the conflict on consumers. Energy costs jumped 12.5% year-over-year, with gasoline prices up 18.9% and fuel oil rising 44.2%, pushing headline CPI to 3.3%. With the average national price of gasoline now at $4.12 per gallon, consumers are feeling pressure.

The encouraging sign, however, is that these higher energy costs have not yet spread to other parts of the economy. Core CPI – which excludes food and energy – rose just 2.6% year-over-year, below expectations, and a narrower “supercore” measure came in at 2.3%. History suggests that once geopolitical tensions are eased, these supply-drive price pressures tend to subside.

The Labor Market is Slowing, But Holding Up

The employment picture is a bit more mixed. March payrolls came in well above expectations at 178,000 new jobs, but the prior month was revised to a loss of 133,000 – a reminder that these reports can be noisy and be subject to varying revisions. The broader trend has been one of gradual slowing, with the economy averaging just 21,000 new jobs per month over the last twelve months, compared to 166,000 per month throughout 2024.

The unemployment rate came down to 4.3%, though this reflects a declining labor force participation rate (now at 61.9%) rather than a surge in hiring. Much of this is structural – with more than 11,000 baby boomers retiring every day, fewer working-age Americans are actively in the workforce.

Diversification Has Paid Off

One of the more important takeaways from 2026 is how well diversification has worked. Eight of the eleven S&P 500 sectors are positive year-to-date, with Energy, Materials, and Industrials among the standout contributors. Compared to the past, returns have not been driven solely by large cap technology stocks. Leadership has come from a variety of areas, reinforcing the value of maintaining a balanced, well-diversified portfolio.

This year has also been a good reminder that staying invested, even through periods of uncertainty, is what allows investors to participate in recoveries like the one we’ve seen over the past several weeks. It took the S&P 500 over two months from its peak in January to fall 10% and less than three weeks to surge back to new all-time highs with a vertical rally of 13%.

Our Perspective

Markets reaching new all-time highs amid an active geopolitical conflict may feel counterintuitive, but it reflects an important truth: over the long run, fundamentals matter most. Earnings remain strong, inflation pressures have yet to broaden meaningfully, and diversified portfolios have held up well through the turbulence. That said, it’s worth acknowledging that markets appear to have priced in a resolution to the conflict that has not yet materialized on the ground. Given how quickly the situation is changing, further volatility is likely — and with it, opportunities for long-term investors to put capital to work at attractive levels.

Our guidance remains consistent: stay focused on your long-term goals, maintain a well-diversified portfolio, and resist the urge to react to every headline. That approach has served investors well through periods of uncertainty, and we believe it remains the right course today.

Respectfully,

Leslie, Matt, Ryan & Ashlee