While some markers of inflation are starting to cool, the labor market is still very tight, and there is a large amount of cash liquidity on household balance sheets as seen in record high levels of bank deposits. It seems likely that elevated inflation and interest rates will persist for a period of time, at least through 2023. Our forecast has been that financial market returns over the next five years to be modestly below long-term historical averages, so we have focused on income generation over growth investing.

Since the sharp COVID recession, while we all enjoyed great market returns and saw our residential property values soar, however growth was too heated and this current transition in valuations is toward more sustainable growth. The Fed is likely not done hiking but they might be able to slow the pace and magnitude of hikes soon.

Since early 2021 we have been shifting our portfolio models toward stable income generation through cash flow generating real estate and preferred equity exposures, mostly tied to real estate, to keep your income levels high when traditional fixed income has been punished by rising rates. Early in 2022, we reduced equity exposures to further push into low correlation income generating investments. During times of high volatility, we don’t have to focus on underlying asset valuations as much as the health and sustainability of cash flows to support your income needs.

Going forward we believe traditional correlations between equities and fixed income will eventually resume and active management will mean reallocating to high quality credit and eventually even high yield. Diversification still rules as our real estate exposure still generates higher returns than bonds. Real estate retains its value in portfolios by creating stability, higher yields and in many cases, tax-sheltered income.

This is not about a recession, at least not yet. Corporate profits continue to grow robustly along while pent-up demand for travel, consumption, investment, borrowing, and the housing market remains solid. Unemployment is at 3.6% while jobs available versus those seeking work is at a multi-decade low. This is about valuation and the reassessment of risk, with the forward price/earnings ratio for US stocks falling from more than 21 times in January to less than 18 today. As markets contemplate a Fed Funds rate discounted to increase to more than 2.5% by year-end, volatility and the positive correlation between stocks and bonds is a particularly challenging combination. Bonds will not, for some time, provide a hedge to stock volatility so real estate that adjusts/raises rents in inflationary times and alternatives that have low or negative correlation are a high priority to all investors. Diversification is more important than ever and real assets and alternatives are places to move and earn cash flows.

We are now in week three of the Russian invasion into Ukraine and the market is still trying to digest the different news stories that are making headlines and fueling volatility. While our thoughts are with the Ukrainian people who have been impacted by a conflict, not of their choosing, we are also focused on how this will affect the global economy, the energy markets, and the Fed’s response.

Since the COVID Recession, the S&P 500 has returned 113.02% (cumulative) from its low point on March 23, 2020 through the end of 2021. During that same period, Optivest clients enjoyed phenomenal returns on their diversified portfolios. In fact, our portfolios, depending on the model risk tolerance, overall experienced the highest returns our portfolios have seen in decades. Thanks to conditions such as ultra-low interest rates and easy money, political deadlock on tax law changes, and gradually improving supply chains, we have benefited from a tremendous rally that brought the stock markets back to all-time highs in an incredibly short period.

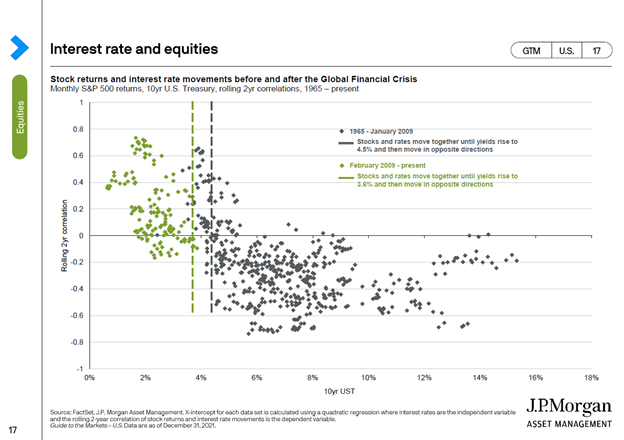

As we approach the end of February, 2022 has seen heightened volatility that has been reminiscent of past corrections and bear markets. US economic data has increasingly indicated more persistent inflation and a tight labor market, both of which have driven the Federal Reserve to take a more hawkish stance. Forecasts for rate hikes have subsequently moved higher and have spooked the markets, especially expensive growth stocks. To make volatility even worse, we have seen numerous headlines over the past few weeks about a possible invasion of Russian forces into Ukraine. We believe the geopolitical tensions have created more noise in the background and we should focus on the issue at-hand, which is a Fed that will have to raise rates multiple times this year. The rate and level of rate increases remains a subject of much debate. Below we outline how the market reacts in a rising-interest rate environment.

In 2021, we made tactical moves in our investment portfolios to underweight US bond exposure, be overweight in real estate and build cash reserves for deployment in 2022 when we see volatility increasing due to headwinds. The US Barclays Agg (a moderate-duration bond index) is -4.31% from its high last year and only faces more losses in face of rising rates. The multi-decade bond rally is indeed over and in reality, it was only briefly interrupted by the pandemic. Our real estate exposure continues to out-perform other asset classes as the interest on leverage is still historically low (and often was refinanced to low fixed-rate over past years) and the asset values appreciate with inflation bringing total returns to the highest levels seen in years. Pensions and institutions continue to invest heavily into real estate in the new bond bear market. In this environment, keen asset selection can make value add purchase and development deals very profitable.

Markets seem primed to equate higher rates as being negative for equities. We’ve seen this before and don’t agree. What really matters is that the Fed is signaling slow and cautious rate hikes, supportive of minimal market impact. This historically muted response to inflation should keep real rates low, in our view, supporting equities and real estate. Stay invested and stay diversified for positive returns occur more frequently over longer periods than negative returns and policy is supportive of high-quality investing. Fundamentals matter.